What Is A Summary Instalment Order

Discover what a Summary Instalment Order (SIO) is in NZ. Learn how this debt management tool can provide a path to financial freedom, protect you from creditors, and offer a fresh start. Expert guidance for South Auckland.

mangerebudgeting.org.nz

What You Will Learn

Discover what a Summary Instalment Order (SIO) is in NZ. Learn how this debt management tool can provide a path to financial freedom, protect you from creditors, and offer a fresh start. Expert guidance for South Auckland.

What Is A Summary Instalment Order: Your Path to Financial Freedom in New Zealand

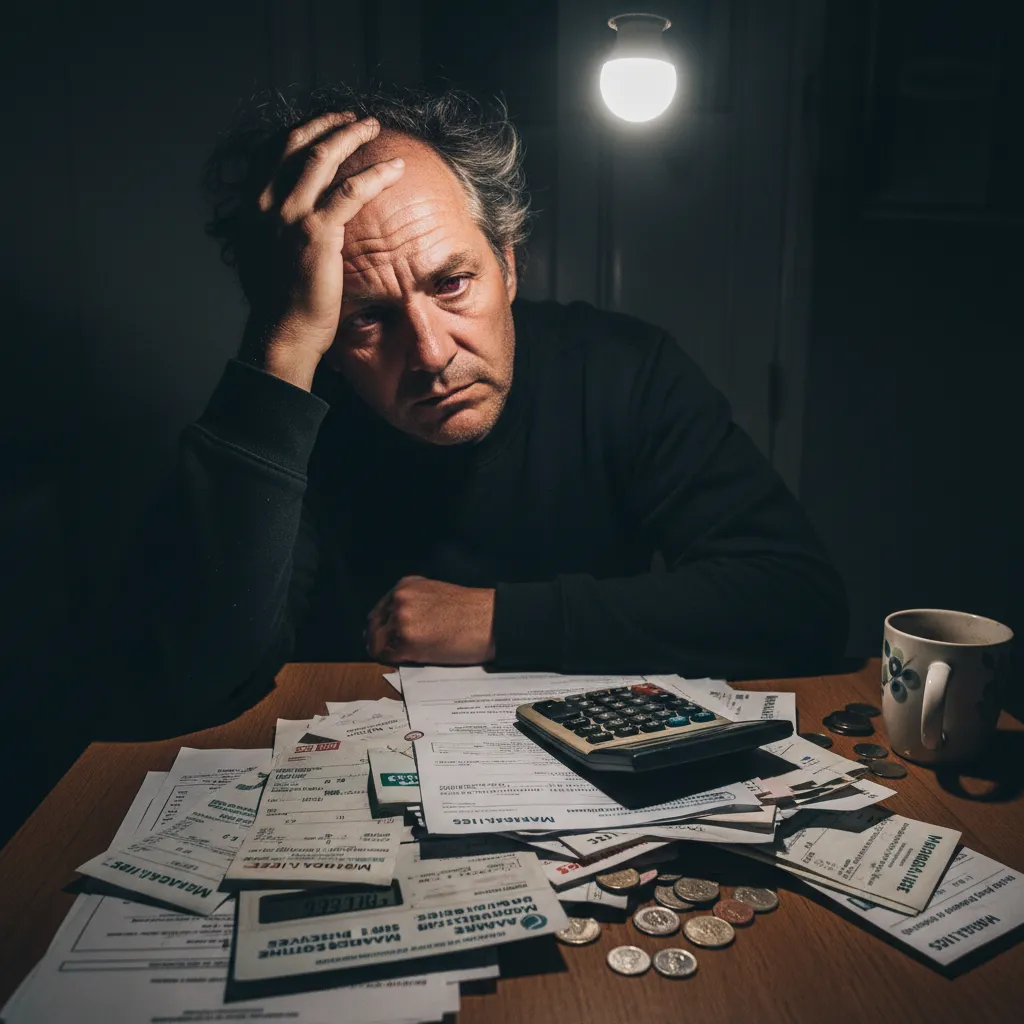

Are you feeling overwhelmed by debt, constantly juggling bills, and seeing no clear way out? The stress of financial hardship can be immense, impacting every aspect of your life. For many New Zealanders, particularly in communities like South Auckland, finding effective debt solutions is a critical step towards regaining control and peace of mind. One powerful tool that can offer significant relief and a structured path to recovery is a Summary Instalment Order (SIO). But what is a Summary Instalment Order, and how can it help you navigate your financial challenges?

This comprehensive guide, brought to you by Mangere Budgeting Services, will demystify the Summary Instalment Order. We’ll explore its definition, benefits, how it works, and how it can serve as a vital stepping stone towards financial resilience. If you’re looking for an authoritative, yet approachable explanation of this essential debt management tool, you’ve come to the right place.

Table of Contents

What is a Summary Instalment Order?

In New Zealand, a Summary Instalment Order (SIO) is a formal, legally binding arrangement for managing unmanageable debt. It’s an alternative to bankruptcy, designed for individuals who owe money but have limited assets and a regular income. Essentially, it allows you to consolidate most of your debts into one manageable repayment plan, overseen by the Official Assignee.

The Insolvency Act 2006 governs Summary Instalment Orders, providing a framework for individuals to get out from under crushing debt while making fair contributions to their creditors based on their ability to pay. It’s particularly beneficial for those who are struggling but committed to fulfilling their financial obligations in a structured manner.

Definition and Purpose

An SIO is a formal debt repayment plan approved by the Official Assignee, a government official responsible for administering insolvencies. Its primary purpose is to provide a structured and controlled environment for debtors to repay their creditors over a period, typically up to three years, without the severe consequences or stigma of bankruptcy. It brings protection from creditors, stopping them from taking further action against you.

“A Summary Instalment Order provides a crucial lifeline for New Zealanders facing insurmountable debt, offering a structured and protected pathway to regain financial stability without resorting to bankruptcy.”

How a Summary Instalment Order Works: A Step-by-Step Guide

Understanding the process is key to determining if a Summary Instalment Order is right for you. While Mangere Budgeting Services can guide you through each step, here’s a general overview:

- Step 1: Initial Consultation and Financial Assessment. Your journey begins with a confidential consultation, often with an approved financial mentor or budgeting service. They will help you assess your financial situation, understand your income, expenses, assets, and liabilities. This crucial step determines if you meet the eligibility criteria for an SIO, which typically involves total unsecured debts between $1,000 and $50,000, and no significant assets.

- Step 2: Application Preparation. If an SIO is deemed appropriate, your mentor will assist you in preparing the application form. This involves gathering all necessary documentation, including details of your creditors, debts, income, and expenditure. Accuracy is paramount here.

- Step 3: Application to the Official Assignee. Once complete, the application is lodged with the Official Assignee. They review your application to ensure it meets all legal requirements and is a viable solution for your circumstances.

- Step 4: Creditor Notification and Proposal. The Official Assignee notifies all your listed creditors about your application. They present a proposal outlining how much you can afford to repay each creditor based on your disposable income. Creditors have an opportunity to object to the proposal or the SIO itself, but valid objections are specific and uncommon if the application is well-prepared.

- Step 5: Order Approval and Repayment Commencement. If approved, the Official Assignee issues the Summary Instalment Order. You will then make regular, affordable payments to the Official Assignee (or a nominated agent, like your budgeting service), who then distributes these funds to your creditors. These payments are fixed for the duration of the SIO.

- Step 6: Completion and Discharge. After successfully completing all payments as per the order, your SIO is discharged, and you are officially free from the included debts. This marks a significant milestone in your financial recovery.

Debts Covered and Not Covered

A Summary Instalment Order covers most unsecured debts. These typically include:

- Credit card debts

- Personal loans

- Overdrafts

- Store cards

- Hire purchase agreements (for items you wish to keep, though these might be treated differently)

- Unpaid utility bills

- Some unpaid rent

However, certain debts are generally not covered:

- Secured debts (e.g., mortgages, car loans where the asset is collateral and you want to keep the asset)

- Student loans

- Child support or maintenance payments

- Fines or court-ordered penalties

- Debts incurred after the SIO is issued

The Role of the Official Assignee

The Official Assignee (part of the Ministry of Business, Innovation & Employment – MBIE) plays a central and impartial role in the Summary Instalment Order process. They:

- Assess your application and financial circumstances.

- Approve or decline the SIO.

- Manage the repayment plan and distribute payments to creditors.

- Provide supervision and support throughout the duration of the order.

- Act as an independent arbiter between you and your creditors.

Key Benefits of a Summary Instalment Order

For individuals grappling with significant debt, a Summary Instalment Order offers a multitude of advantages, making it a powerful tool for financial recovery:

- Protection from Creditors: Once an SIO is in place, creditors cannot pursue you directly for outstanding debts included in the order. This means no more threatening letters, phone calls, or legal actions, providing immediate peace of mind.

- Structured, Affordable Repayments: The SIO consolidates most of your unsecured debts into one manageable payment. This payment is determined based on what you can realistically afford, ensuring the plan is sustainable and helps you budget effectively.

- Avoids Bankruptcy: An SIO is a less severe form of insolvency than bankruptcy. While both affect your credit rating, an SIO has fewer restrictions and is generally perceived as a more proactive and responsible way to address debt.

- Clear End Date: The order has a defined term, usually up to three years. Knowing there’s a clear end in sight can be incredibly motivating and helps you plan for a debt-free future.

- Financial Education and Support: Many individuals applying for an SIO work closely with financial mentors. This provides an invaluable opportunity to learn better money management skills, budgeting techniques, and strategies for long-term financial resilience.

- Reduced Stress and Anxiety: The biggest benefit for many is the significant reduction in stress and anxiety that comes from having a clear plan and legal protection. It allows you to focus on rebuilding your life rather than constantly worrying about debt.

Understanding the Impact: What Happens During an SIO?

While a Summary Instalment Order provides immense relief, it’s also important to understand its practical implications during its term. Transparency about these aspects is crucial for making an informed decision:

- Credit Rating Impact: An SIO will be noted on your credit report, affecting your ability to obtain new credit for the duration of the order and for a period after discharge. This is a temporary consequence, but an important one to consider.

- Financial Discipline: Adhering to the repayment schedule is mandatory. Any changes to your income or expenses must be communicated to the Official Assignee. The SIO encourages strict budgeting and financial discipline.

- Restrictions on New Debt: During the term of the SIO, you generally cannot incur new debts exceeding a certain threshold (e.g., $1,000) without the permission of the Official Assignee. This helps prevent further financial distress.

- Asset Protection: Unlike bankruptcy, an SIO usually allows you to keep essential assets, such as your car or household goods, as long as they are not deemed excessive or subject to secured loans.

- Support System: Throughout the SIO, you are not alone. Resources like Mangere Budgeting Services can provide ongoing support, advice, and financial education, ensuring you stay on track and emerge financially stronger.

Conclusion

Understanding what is a Summary Instalment Order is the first step towards taking control of your financial future. It represents a structured, legal, and dignified alternative for New Zealanders struggling with unmanageable debt, offering a clear path to repayment and a fresh start without the full impact of bankruptcy.

If you are in South Auckland and facing financial difficulties, Mangere Budgeting Services is here to help. Our experienced financial mentors can provide confidential advice, assess your eligibility for a Summary Instalment Order, and guide you through every step of the application process. Don’t let debt define your future. Reach out today and explore how an SIO, coupled with expert guidance, can help you achieve financial resilience and peace of mind.

Frequently Asked Questions (FAQ)

- What kind of debts can be included in a Summary Instalment Order?

Most unsecured debts such as credit card balances, personal loans, overdrafts, store cards, and unpaid utility bills can be included. Secured debts (like mortgages) and specific obligations like student loans, child support, or fines are generally not included.

- How long does a Summary Instalment Order last?

A Summary Instalment Order typically lasts for a period of up to three years. The exact duration depends on your financial situation and the repayment plan agreed upon with the Official Assignee.

- Will a Summary Instalment Order affect my credit rating?

Yes, an SIO will be recorded on your credit report and will affect your credit rating. This impact usually lasts for the duration of the order and for a period afterwards, making it more challenging to obtain new credit during this time. However, it is often viewed more favorably than bankruptcy.

- Can I apply for a Summary Instalment Order if I own a house?

Eligibility for an SIO depends on your total unsecured debt (usually up to $50,000) and your assets. If you own a house, especially if it has significant equity, you may not be eligible for an SIO as you might have assets that could be used to repay your debts. The Official Assignee will assess your full financial situation.

- What happens if I miss a payment under an SIO?

Missing a payment can jeopardize your Summary Instalment Order. It’s crucial to contact the Official Assignee or your financial mentor immediately if you anticipate or miss a payment. Persistent missed payments can lead to the cancellation of the SIO, leaving you vulnerable to creditors again.

- Who can help me apply for a Summary Instalment Order?

Approved financial mentors, budgeting services (like Mangere Budgeting Services), or a lawyer specializing in insolvency can help you assess your eligibility, prepare your application, and guide you through the Summary Instalment Order process.

References/Sources

- New Zealand Legislation. (2006). Insolvency Act 2006. Retrieved from legislation.govt.nz

- Ministry of Business, Innovation & Employment (MBIE). (n.d.). Summary Instalment Order. Retrieved from insolvency.govt.nz

- Financial Mentors New Zealand. (n.d.). Finding a Financial Mentor. Retrieved from finmen.org.nz

- Citizens Advice Bureau NZ. (n.d.). Debt solutions and insolvency. Retrieved from cab.org.nz