Managing Overdue Bills and Avoiding Fines

Learn how to manage overdue bills in NZ effectively, avoid fines, and prevent future financial stress. This guide for South Auckland covers prioritising, communicating, and setting up payment plans.

mangerebudgeting.org.nz

What You Will Learn

Learn how to manage overdue bills in NZ effectively, avoid fines, and prevent future financial stress. This guide for South Auckland covers prioritising, communicating, and setting up payment plans.

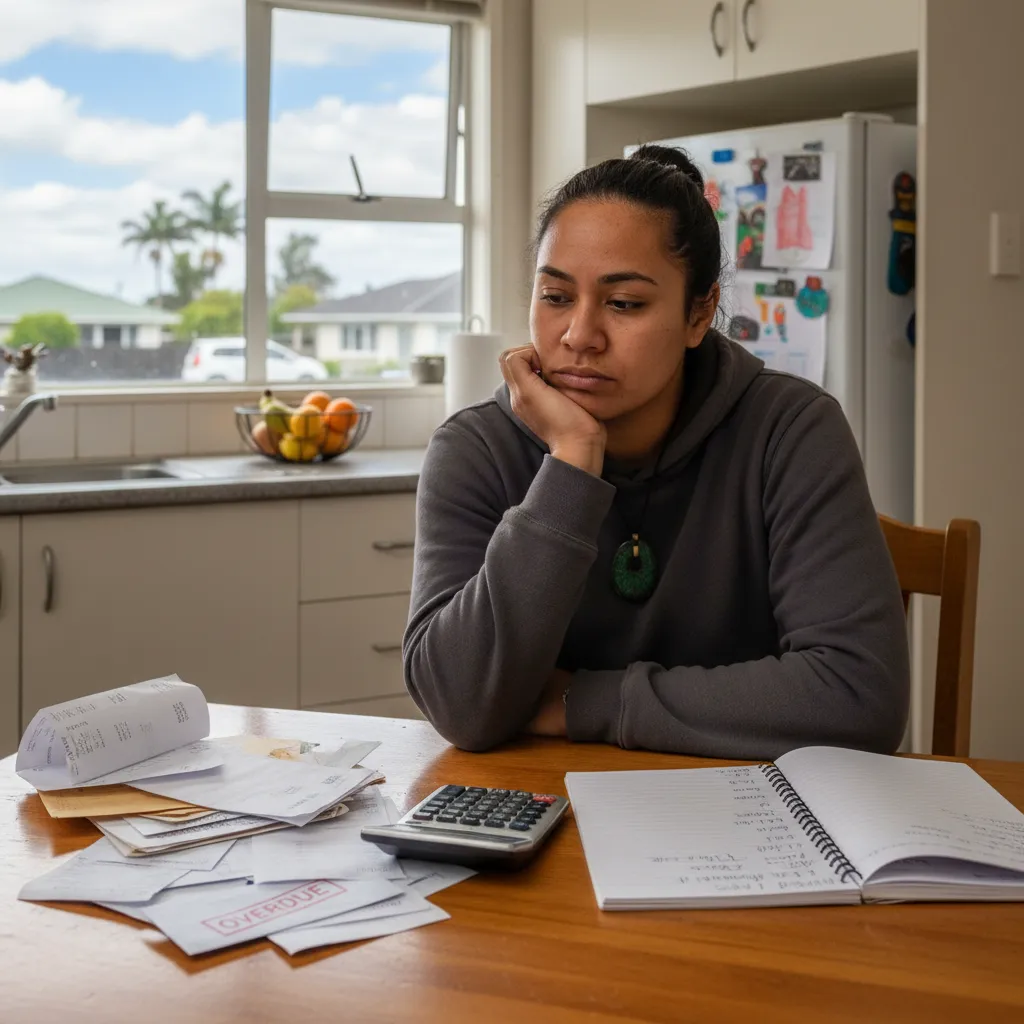

Facing a pile of overdue bills can feel overwhelming, especially when you’re juggling daily expenses and trying to make ends meet in places like South Auckland. It’s a common challenge many New Zealanders face, but you don’t have to navigate it alone. This comprehensive guide will equip you with practical strategies on how to manage overdue bills NZ-style, helping you avoid hefty fines, protect your credit rating, and regain control of your financial well-being. From prioritising what to pay first to setting up manageable payment plans, we’ll walk you through actionable steps to turn stress into stability.

1. Prioritising Bills Effectively

When money is tight, the first step to managing overdue payments is to identify which bills are most critical. Not all debts carry the same weight or have the same immediate consequences. A common strategy is to classify your bills into ‘essential’ and ‘non-essential’, and then prioritise based on the severity of the repercussions for non-payment.

Understanding Urgency and Impact

- Life Essentials: These are your absolute priorities. They include rent or mortgage payments (to keep a roof over your head), electricity, gas, and water (essential utilities), and food. Non-payment here can lead to homelessness, disconnection of vital services, or severe health risks.

- Secured Debt: Loans where an asset is used as collateral (e.g., a car loan where the car is the security). Missing payments can lead to repossession of the asset.

- Unsecured Debt: Debts like credit cards, personal loans, or store credit. While these can accrue significant interest and negatively impact your credit score, the immediate threat to your living situation or essential services is generally lower than with essential bills or secured debts.

- Fines & Penalties: Parking tickets, speeding fines, etc., can escalate if unpaid, but usually don’t carry the same immediate threat as essential bills.

A smart way to visualise your financial situation is to create a simple spreadsheet or use a budgeting app. List all your income and outgoings, noting due dates and minimum payments. This clarity is crucial when you’re working out how to manage overdue bills NZ households often face.

Once you have a clear picture, focus on allocating funds to your highest priority bills first. Even making a partial payment on an essential bill is often better than no payment at all, as it shows commitment and may prevent immediate severe action.

2. Communicating with Service Providers

Ignoring an overdue bill is the worst thing you can do. Most companies prefer to work with you to recover funds rather than resorting to debt collectors or legal action. Proactive communication is key to finding a solution and demonstrating your commitment to resolve the issue.

Step-by-Step Approach to Contacting Creditors

- Gather All Information: Before calling, have your account number, the bill amount, the due date, and a brief explanation of your financial situation ready. Knowing your current income and essential expenses will also be helpful.

- Be Honest and Clear: Explain your situation concisely. Are you facing temporary hardship due to illness, job loss, or an unexpected expense? Most providers are understanding if approached respectfully and with honesty.

- State Your Intent: Clearly state that you want to resolve the outstanding payment and are looking for options. Ask about payment extensions, hardship policies, or payment plans.

- Document Everything: Note down the date and time of your call, the name of the person you spoke to, what was agreed upon, and any reference numbers. Follow up with an email if possible to have a written record.

Remember, it’s always easier to talk to a provider when a bill is just overdue or about to become overdue, rather than months down the line when it’s been passed to a debt collection agency. Many utility companies in New Zealand have specific hardship policies designed to help customers.

3. Setting Up Payment Plans

Once you’ve made contact, the next logical step is to explore setting up a realistic payment plan. This can help you spread the cost of an overdue bill over several weeks or months, making it more manageable within your budget.

Negotiating a Realistic Payment Arrangement

- Temporary Hardship Agreements: Many service providers and lenders offer specific ‘hardship’ provisions. This might involve temporarily reducing your payments, pausing payments, or waiving late fees. You’ll likely need to provide proof of your financial situation.

- Flexible Payment Schedules: If you can’t pay the full amount immediately, ask if you can pay in smaller, more frequent installments. For example, weekly or fortnightly payments might fit better with your income cycle than one large monthly sum.

- Consider Interest Waivers: For some debts, particularly credit card or personal loan arrears, you might be able to negotiate a temporary freeze or reduction in interest payments while you catch up. This can significantly reduce the total amount you owe over time.

Before agreeing to any plan, ensure it’s genuinely affordable. Work out exactly how much you can realistically pay each week or month without falling behind on other essential bills. A payment plan that you can’t stick to is ultimately unhelpful and can damage trust with your creditor.

4. Consequences of Unpaid Bills

Understanding the potential ramifications of not paying your bills can motivate you to take action and seek solutions. The consequences can range from minor fees to significant impacts on your future financial opportunities.

Impact on Your Financial Future in New Zealand

- Late Payment Fees & Penalties: Most companies will charge additional fees for overdue payments. These can quickly add up, making the original bill even harder to clear.

- Negative Credit Rating: Unpaid debts are reported to credit bureaus. A poor credit rating can make it difficult to get future loans, mortgages, rental agreements, or even new utility connections. This significantly impacts your ability to access credit in New Zealand.

- Debt Collection Agencies: If a bill remains unpaid for an extended period, the original company may sell the debt to a collection agency. Dealing with debt collectors can be stressful, though they must adhere to specific regulations in NZ.

- Legal Action & Repossession: For significant debts, especially secured ones, creditors can take legal action, leading to court judgments, wage garnishment, or the repossession of assets (like a car).

- Disconnection of Services: Utility companies can disconnect your power, gas, or internet if bills go unpaid, causing immediate disruption to your household.

Stat Callout: