How To Get Out Of Car Finance Debt Nz

Struggling with car finance debt in NZ? Learn how to get out of car finance debt NZ with expert strategies, budgeting tips, and resources from Mangere Budgeting Services.

mangerebudgeting.org.nz

What You Will Learn

Struggling with car finance debt in NZ? Learn how to get out of car finance debt NZ with expert strategies, budgeting tips, and resources from Mangere Budgeting Services.

Introduction: Navigating Your Way Out of Car Finance Debt in NZ

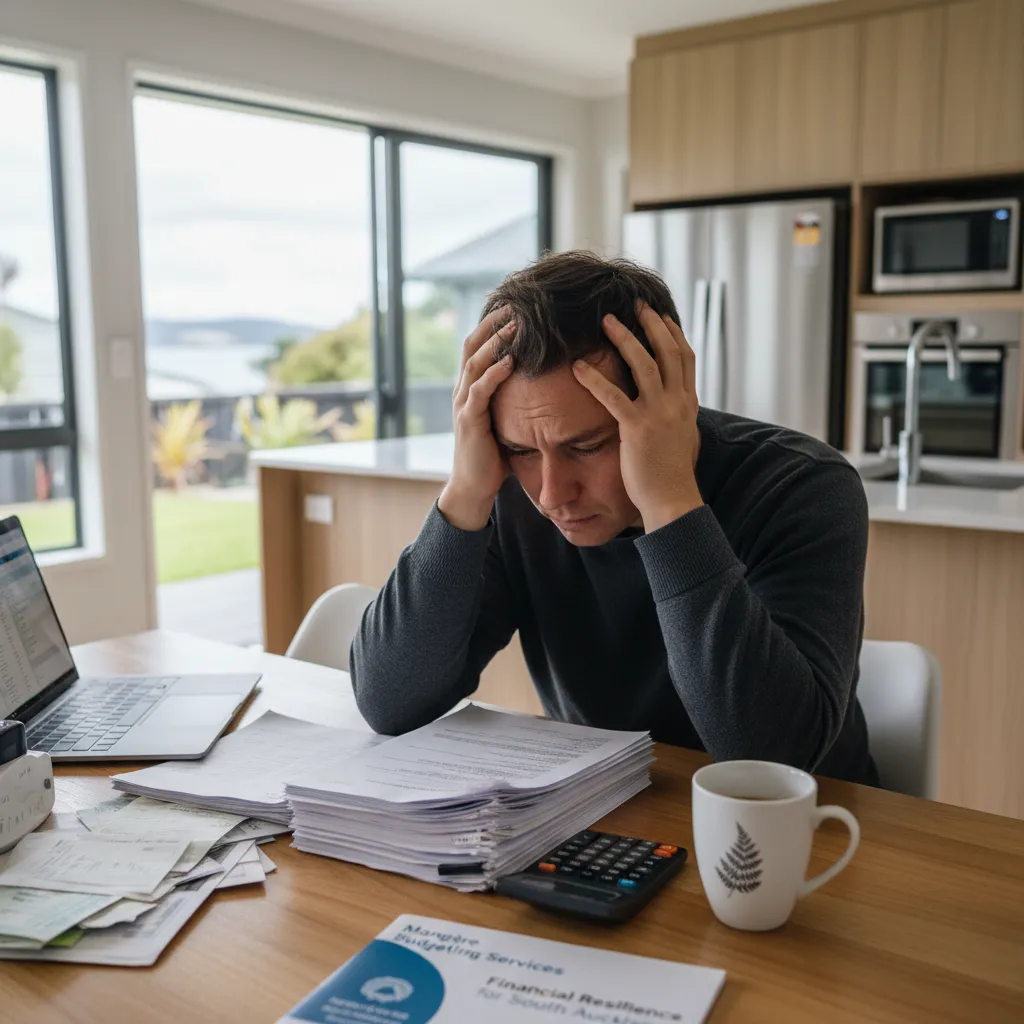

The freedom a car provides in New Zealand, especially across South Auckland, is undeniable. It’s often essential for work, family, and daily life. However, for many, the dream of car ownership can quickly turn into a financial burden, leaving them trapped in a cycle of car finance debt. If you’re currently asking, “how to get out of car finance debt NZ?”, you’re not alone. This comprehensive guide is designed to empower you with the knowledge and actionable steps needed to regain control of your finances and break free from car loan stress.

We understand the unique challenges faced by New Zealanders, and particularly those in communities like Mangere, where financial resilience is key. This article will walk you through understanding your debt, exploring practical solutions, and connecting you with resources that can help. Let’s drive towards a debt-free future together.

Table of Contents

- Understanding Car Finance Debt in New Zealand

- Strategies to Get Out of Car Finance Debt in NZ

- Action Checklist: Your Path to Debt-Free Driving

- Conclusion: Taking the Wheel of Your Financial Future

- Frequently Asked Questions About Car Finance Debt in NZ

- References/Sources

Understanding Car Finance Debt in New Zealand

Car finance debt in NZ often stems from various factors, including high-interest rates, unforeseen expenses, job loss, or simply overextending oneself. It’s crucial to acknowledge the reality of your situation without judgment. Many New Zealanders find themselves in this predicament, and understanding the nature of the debt is the first step towards resolving it.

“Ignorance of your financial position is not bliss; it’s a barrier to financial freedom. Take the time to understand every dollar you owe.”

Common pitfalls include accepting predatory loan terms, not fully comprehending the total cost of the loan (interest + principal + fees), and not accounting for additional car ownership costs like insurance, registration, and maintenance. The impact of unmanaged car debt can be significant, affecting your credit score, limiting future borrowing capacity, and causing immense stress.

Strategies to Get Out of Car Finance Debt in NZ

Getting out of car finance debt requires a strategic approach. Here are actionable steps you can take, tailored for the New Zealand context.

Step 1: Assess Your Current Financial Situation

Before you can tackle your debt, you need a clear picture of where you stand. Gather all your financial documents: loan agreements, bank statements, income details, and a list of all your expenses. Calculate your total car loan balance, remaining term, and current interest rate. This clarity will be your foundation.

Step 2: Understand Your Car Loan Agreement

Deep dive into the fine print of your car finance agreement. Look for details regarding early repayment penalties, fees for missed payments, and terms around voluntary surrender. Knowing these clauses will help you avoid additional costs and make informed decisions.

Step 3: Explore Repayment Options

- Refinancing: If your credit score has improved or interest rates have dropped, you might qualify for a new loan with a lower interest rate or more manageable terms. This could significantly reduce your monthly payments and total interest paid.

- Debt Consolidation: Combining your car loan with other debts into a single, new loan (potentially a personal loan or a home equity loan if you own property) can simplify payments and potentially lower your overall interest rate. However, ensure the new loan terms are genuinely better.

- Voluntary Surrender: As a last resort, if payments are truly unsustainable, you might consider voluntarily surrendering the vehicle. Be aware that this can negatively impact your credit score, and you may still be liable for any shortfall between the sale price of the car and the outstanding loan balance, plus associated fees.

- Selling the Car: If the car’s market value is higher than your outstanding loan balance, selling it could be a viable option to clear the debt entirely. If you owe more than it’s worth, you’d need to cover the difference.

Step 4: Create a Budget and Cut Expenses

A rigorous budget is your most powerful tool. Track every dollar you spend and identify areas where you can cut back. Even small savings on daily coffees, takeaways, or subscriptions can add up to significant amounts that can be directed towards your car loan. Consider a temporary ‘no-spend’ challenge to accelerate your debt repayment.

Step 5: Seek Professional Financial Advice

Organisations like Mangere Budgeting Services offer invaluable, free and confidential support. They can help you create a realistic budget, negotiate with creditors on your behalf, and explore all available debt management options. Don’t hesitate to reach out for expert guidance; it’s a sign of strength, not weakness.

Step 6: Negotiate with Your Lender

If you’re struggling to make payments, contact your lender immediately. They may be willing to work with you to find a solution, such as a temporary payment holiday, reduced payments for a period, or a restructured payment plan. Honesty and proactive communication are key.

Action Checklist: Your Path to Debt-Free Driving

Use this checklist to guide your journey out of car finance debt:

-

Gather All Loan Documents: Compile your car loan agreement, recent statements, and payment history.

-

Calculate Total Debt: Determine your exact outstanding balance, interest rate, and remaining term.

-

Review Your Budget: Create or update a detailed budget, identifying all income and expenses.

-

Identify Areas for Cost Cutting: Pinpoint non-essential spending that can be reduced or eliminated.

-

Research Refinancing Options: Check if you qualify for a lower interest rate loan from another provider.

-

Contact Mangere Budgeting Services (or similar): Schedule a free consultation to discuss your situation and options.

-

Communicate with Your Lender: If experiencing hardship, discuss potential payment solutions with them before missing payments.

-

Consider Selling or Downsizing: Evaluate if selling your current vehicle for a cheaper one is a viable solution.

-

Automate Extra Payments: Set up automatic transfers for any extra money you can put towards the principal.

-

Monitor Your Progress: Regularly review your budget and debt repayment plan to stay on track.

Conclusion: Taking the Wheel of Your Financial Future

Getting out of car finance debt in New Zealand is a challenging but achievable goal. It requires dedication, smart planning, and sometimes, the courage to ask for help. By systematically assessing your situation, understanding your options, and taking decisive action, you can move towards financial freedom and alleviate the stress that debt often brings.

Remember, organisations like Mangere Budgeting Services are here to support your journey towards financial resilience. Don’t let car debt define your future; take the wheel and steer yourself towards a brighter, debt-free tomorrow.

Frequently Asked Questions About Car Finance Debt in NZ

What happens if I can’t pay my car finance in NZ?

If you can’t pay your car finance, it’s crucial to contact your lender immediately. They may offer options like a payment holiday or a restructured plan. If you default, the lender can repossess your vehicle, and you could still be liable for any outstanding balance after the sale, plus fees. This will also negatively impact your credit score.

Can I refinance my car loan with bad credit in NZ?

Refinancing with bad credit can be challenging but not impossible. Some lenders specialise in bad credit loans, but they often come with higher interest rates. It’s best to improve your credit score first, if possible, or seek advice from a budgeting service to explore all options, including debt consolidation, which might be a better fit.

Is voluntary surrender a good option for car finance debt in NZ?

Voluntary surrender should generally be considered a last resort. While it removes the burden of payments, it severely impacts your credit rating. You may also still owe a ‘shortfall’ amount if the vehicle sells for less than your outstanding debt, and the lender can pursue you for this amount. Always seek financial advice before making such a decision.

How can Mangere Budgeting Services help me with car finance debt?

Mangere Budgeting Services offers free, confidential financial advice. They can help you create a budget, negotiate with creditors, explore debt management plans, and provide guidance on understanding your loan terms. Their expertise can be invaluable in finding a sustainable path out of car finance debt.

What are the alternatives to a car loan if I need a vehicle?

Consider purchasing a cheaper, reliable used car outright with savings, using public transport, car-sharing services, or cycling if feasible. For essential needs, some community organisations offer low-interest vehicle loans. Always explore all options to avoid getting into high-interest debt.

References/Sources