Debt Management & Financial Resilience

Expert debt help NZ. Understand debt types, learn reduction strategies, avoid high-interest loans, and find free counselling. Reclaim financial resilience.

mangerebudgeting.org.nz

What You Will Learn

Expert debt help NZ. Understand debt types, learn reduction strategies, avoid high-interest loans, and find free counselling. Reclaim financial resilience.

Debt Management & Financial Resilience: Your Guide to Debt Help NZ

Navigating financial challenges can feel overwhelming, especially when debt starts to pile up. In New Zealand, many individuals and families grapple with various forms of debt, from credit cards to personal loans, often feeling trapped in a cycle that seems impossible to break. But there is hope, and expert debt help NZ services are readily available to guide you towards a brighter financial future.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to understand, manage, and ultimately overcome debt. We’ll explore different debt types, practical reduction techniques, pitfalls to avoid, and how professional debt counselling can provide the crucial support you need for long-term financial resilience. Let’s embark on this journey together to reclaim control of your finances.

Table of Contents

Understanding Different Types of Debt

Before tackling debt, it’s crucial to understand its various forms. Not all debt is created equal, and knowing the distinctions can help you prioritise and strategise your repayment plan effectively. Here in New Zealand, you’ll encounter a range of common debt types.

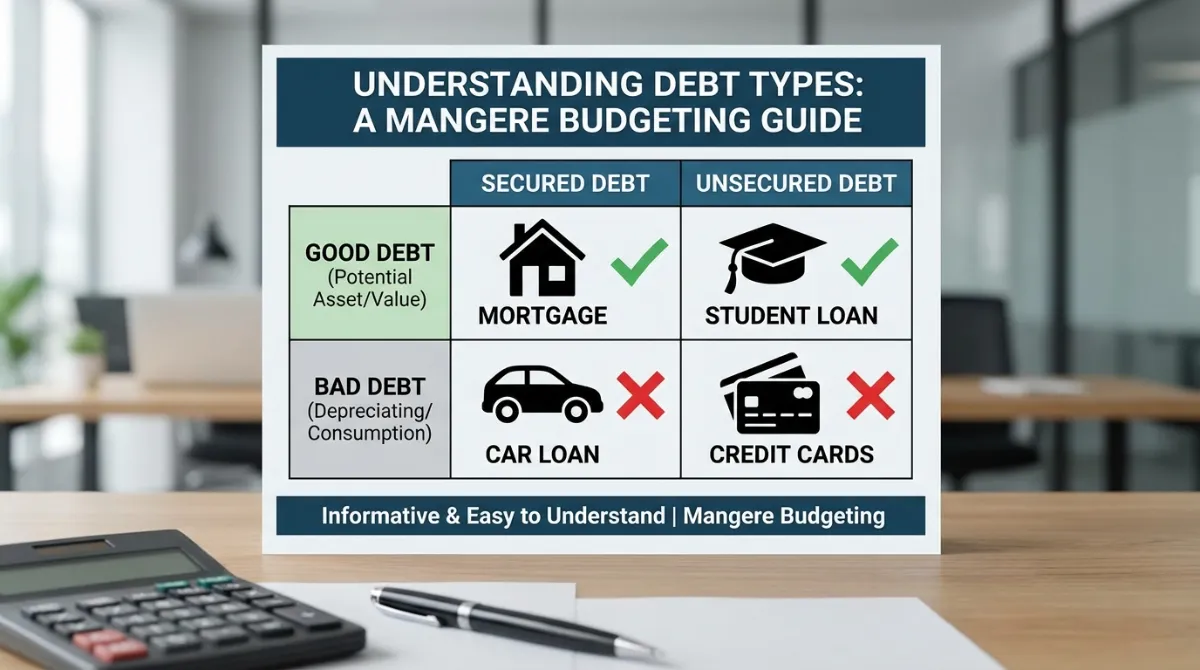

Secured vs. Unsecured Debt

- Secured Debt: This type of debt is backed by an asset, such as a house (mortgage) or a car (car loan). If you default on payments, the lender can seize the asset. Interest rates are typically lower due to reduced risk for the lender.

- Unsecured Debt: Not backed by any asset, making it riskier for lenders and often resulting in higher interest rates. Examples include credit cards, personal loans, and store finance.

Good Debt vs. Bad Debt

While often debated, some debt can be seen as “good” if it helps you build wealth or increases your future income potential, such as a student loan for higher education or a mortgage on a primary residence. “Bad” debt typically depreciates in value or comes with exorbitant interest rates, like high-interest credit card balances for non-essential purchases.

Common Debt Types in NZ

- Credit Card Debt: High-interest, revolving debt that can quickly spiral out of control if not managed responsibly.

- Personal Loans: Often used for larger purchases or consolidating smaller debts, with fixed repayment terms.

- Car Loans: Secured against the vehicle, crucial for many Kiwis but needs careful budgeting.

- Student Loans: Interest-free for borrowers residing in New Zealand, making them a more manageable debt, though still a financial commitment.

- Hire Purchase & Store Finance: Often come with deferred payment options but can carry very high-interest rates if introductory periods are missed.

“Understanding the nature of your debt is the first critical step towards regaining control. It’s not just about the amount, but also the terms, interest rates, and the impact on your overall financial health.”

📊 Stat Callout: Recent data indicates that New Zealand household debt reached a record high of 165% of net disposable income in 2023, highlighting the widespread need for effective debt help NZ strategies.

Strategies for Debt Reduction

Once you understand your debt landscape, the next step is to implement practical strategies to reduce what you owe. This isn’t just about paying more; it’s about smart, consistent effort. Here are proven methods for effective debt help NZ.

1. Create a Detailed Budget

A budget is your financial roadmap. It helps you track income and expenses, identify where your money is going, and find areas to cut back. This frees up funds to put towards debt. Be realistic and consistent.

2. Prioritise Debts (Snowball or Avalanche Method)

- Debt Snowball: Pay off your smallest debt first, regardless of interest rate, while making minimum payments on others. The psychological boost from clearing a debt motivates you to continue.

- Debt Avalanche: Focus on paying off the debt with the highest interest rate first. This method saves you the most money in the long run.

3. Consider Debt Consolidation

Consolidating multiple debts into a single loan, often with a lower interest rate, can simplify payments and potentially reduce your overall cost. This might be a personal loan or a balance transfer credit card. Be cautious and ensure the new terms are genuinely better.

4. Negotiate with Creditors

Many creditors are willing to work with you if you’re struggling. Don’t be afraid to contact them to discuss options like payment plans, reduced interest rates, or even partial debt forgiveness. Open communication is key.

5. Increase Your Income (Temporarily or Permanently)

Exploring ways to boost your income, even temporarily, can significantly accelerate debt repayment. This could involve side hustles, selling unused items, or asking for a raise.

✔️ Action Checklist for Debt Reduction

- ☐ List all your debts: creditor, balance, interest rate, minimum payment.

- ☐ Create a realistic monthly budget and stick to it.

- ☐ Choose either the debt snowball or avalanche method.

- ☐ Automate debt payments to avoid missing due dates.

- ☐ Explore opportunities to earn extra income.

- ☐ Reduce unnecessary expenses (e.g., subscriptions, eating out).

- ☐ Avoid taking on new debt while you’re repaying existing ones.

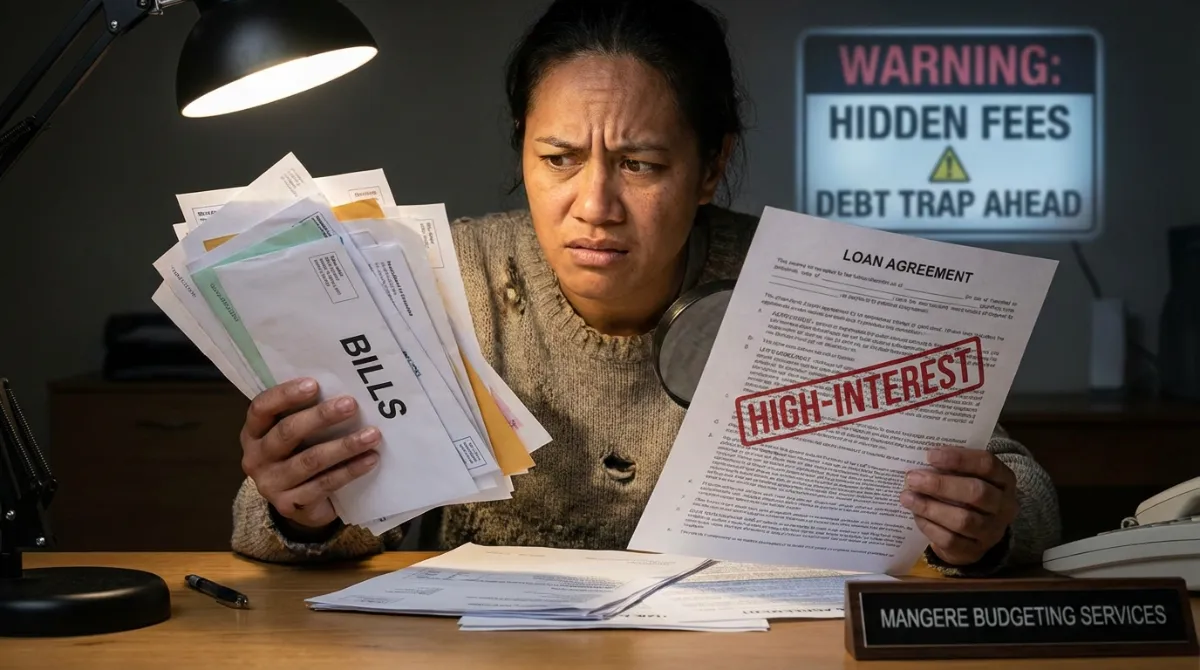

Avoiding Payday Loans & High-Interest Debt

When financial emergencies strike, the temptation to turn to quick-fix solutions like payday loans can be strong. However, these often lead to a deeper debt trap. Understanding the risks and knowing alternatives is vital for your financial resilience and a core component of effective debt help NZ.

The Dangers of Predatory Lending

Payday loans and some other forms of high-interest credit are designed for short-term needs but come with extremely high Annual Percentage Rates (APRs) – sometimes in the hundreds or even thousands of percent. They can quickly turn a small emergency into an insurmountable debt burden, leading to a cycle of borrowing to pay off previous loans.

- Exorbitant Fees: Beyond high interest, many predatory loans include hidden fees, late payment charges, and refinancing costs.

- Debt Spiral: The short repayment terms often make it impossible for borrowers to pay back the full amount, forcing them to roll over the loan or take out new ones, trapping them in a cycle.

- Stress & Harassment: Aggressive collection tactics can add immense psychological stress to an already difficult situation.

Smarter Alternatives to High-Interest Loans

Instead of turning to predatory lenders, consider these safer options:

- Budgeting Services: Organisations like Mangere Budgeting can help you create a sustainable budget and explore options.

- Community Lending: Some non-profits offer low or no-interest loans for essential expenses, providing a compassionate form of debt help NZ.

- Emergency Fund: Building even a small emergency fund can act as a buffer against unexpected costs.

- Talking to Creditors: As mentioned, communicating with existing creditors about payment plans can prevent the need for new, risky loans.

- Advance from Employer: If possible, ask your employer for an advance on your wages.

“The ‘quick fix’ of a payday loan often leads to a long-term financial nightmare. Prioritise sustainable solutions and seek professional advice.”

Accessing Debt Counselling Services

Sometimes, despite your best efforts, managing debt can feel insurmountable alone. This is where professional debt help NZ through budgeting and debt counselling services becomes invaluable. Organisations like Mangere Budgeting provide crucial, impartial support and expert guidance.

What Debt Counselling Offers

- Personalised Budgeting: Counsellors help you create a realistic budget tailored to your income and expenses.

- Debt Management Plans (DMPs): They can negotiate with your creditors on your behalf to reduce payments, freeze interest, or waive fees, consolidating your debts into one manageable repayment plan.

- Advocacy: Acting as an intermediary between you and your creditors, reducing stress and ensuring fair treatment.

- Financial Education: Equipping you with the skills and knowledge for long-term financial independence.

- Support & Empathy: Providing a non-judgmental space to discuss your financial worries and work towards solutions.

Why Choose Professional Debt Help NZ?

While DIY approaches are commendable, a professional can offer perspectives and leverage that individuals often lack. They understand the intricacies of consumer law in New Zealand and have established relationships with creditors, often achieving outcomes that would be difficult to secure on your own.

Seeking help is a sign of strength, not weakness. If you’re struggling, don’t delay. Reach out to a reputable budgeting service in your community to explore your options and take the first step towards financial freedom.

Reclaiming Your Financial Future

Debt can be a heavy burden, but it doesn’t have to define your life. By understanding its different forms, implementing smart reduction strategies, avoiding predatory loans, and most importantly, knowing when and how to access professional debt help NZ, you can navigate your way to financial resilience.

Remember, every journey begins with a single step. Take that step today by assessing your financial situation and reaching out to a trusted budgeting service. With expert guidance and a commitment to change, you can achieve financial stability and peace of mind. Your future self will thank you.

Frequently Asked Questions (FAQ)

Q: What is the best way to get rid of debt fast in NZ?

A: The “best” way depends on your situation. For many, a combination of strict budgeting, choosing between the debt snowball (psychological wins) or debt avalanche (financial savings) method, and potentially debt consolidation or seeking professional debt help NZ through a budgeting service can accelerate repayment. Increasing income and reducing expenses are also key.

Q: Can debt counselling services in NZ really help me?

A: Yes, absolutely. Reputable debt counselling services in NZ, often community-based and free, can provide invaluable assistance. They help create realistic budgets, negotiate with creditors on your behalf, develop debt management plans, and offer financial education to prevent future debt issues. They provide tailored debt help NZ solutions.

Q: What are the risks of using a payday loan in New Zealand?

A: Payday loans in NZ carry significant risks due to their extremely high interest rates and short repayment periods. They can trap borrowers in a debt spiral, where they borrow more just to pay off previous loans, leading to mounting fees and an overwhelming financial burden. Always explore alternatives like budgeting services or community lending before considering a payday loan.

Q: Is a student loan considered “bad debt” in NZ?

A: In New Zealand, student loans are generally considered “good debt” for most residents. They are interest-free if you remain in NZ, and repayment terms are tied to your income, making them manageable. They represent an investment in your education and future earning potential, which distinguishes them from high-interest consumer debt.

References/Sources

- Reserve Bank of New Zealand. (2023). Household Debt Statistics and Financial Stability Report.

- Financial Services Complaints Limited (FSCL). (Ongoing). Understanding Your Rights and Obligations.

- Citizens Advice Bureau (CAB) New Zealand. (Ongoing). Debt and Money Management Advice.

- MoneyTalks. (Ongoing). Free and Confidential Financial Mentoring.

- Sorted.org.nz. (Ongoing). Your independent guide to managing your money.