Debt Management & Relief

Struggling with debt in South Auckland? Get expert, approachable debt help & discover clear pathways to financial relief. Learn strategies, avoid predatory lenders, & find local support.

mangerebudgeting.org.nz

What You Will Learn

Struggling with debt in South Auckland? Get expert, approachable debt help & discover clear pathways to financial relief. Learn strategies, avoid predatory lenders, & find local support.

Feeling overwhelmed by debt? You’re not alone. Many individuals and families in South Auckland face financial challenges, and understanding how to navigate debt can feel daunting. But there is hope, and there are clear pathways to regaining control of your finances. This comprehensive guide is designed to provide you with expert, approachable debt help South Auckland residents can trust, covering everything from identifying the types of debt to actionable strategies for relief.

We believe that financial literacy empowers communities. By understanding your options and accessing the right resources, you can move towards a more stable and secure financial future. Let’s explore effective debt management and relief strategies together.

Table of Contents

Understanding Different Types of Debt

Not all debt is created equal. Recognising the nature of your debt is the first step towards managing it effectively. Generally, debt can be categorised by whether it is secured or unsecured, and by its purpose.

- Secured Debt: This type of debt is ‘secured’ by an asset, meaning if you fail to make payments, the lender can repossess that asset. Examples include mortgages (secured by your home) and car loans (secured by your vehicle). While these often have lower interest rates, defaulting carries significant risks.

- Unsecured Debt: This debt is not tied to a specific asset, making it riskier for lenders and often resulting in higher interest rates. Common examples include credit card debt, personal loans, medical bills, and payday loans. These are frequently a source of financial stress for those seeking debt help South Auckland.

- Good vs. Bad Debt: Debt for investments that appreciate in value or increase your earning potential (like a home loan or student loan for education) can be considered ‘good’ debt. ‘Bad’ debt, conversely, is for depreciating assets or consumption, especially at high interest rates (e.g., credit card debt on consumer goods).

Understanding these distinctions helps you prioritise and strategise your debt repayment, focusing first on high-interest, unsecured debts that offer the least financial benefit and the most stress.

Signs of Financial Distress

Identifying the early warning signs of financial distress is crucial. The sooner you recognise them, the quicker you can seek effective debt help South Auckland resources offer. Ignoring these signals can lead to a spiralling debt cycle.

- Making Only Minimum Payments: If you’re consistently only paying the minimum on credit cards or loans, your debt isn’t reducing significantly, and interest charges are accumulating.

- Borrowing to Pay Bills: Relying on new loans, credit cards, or overdrafts to cover essential living expenses or existing debt payments is a critical red flag.

- Stress and Anxiety About Money: Constant worry, sleepless nights, or arguments about finances are strong indicators that your debt is impacting your well-being.

- Avoiding Opening Bills or Answering Calls: A natural but ultimately detrimental reaction to financial pressure.

- Using Savings for Everyday Expenses: Depleting your emergency fund or long-term savings to cover short-term costs.

- Being Denied for Credit: This could indicate your credit score has suffered due to previous financial difficulties.

If any of these signs resonate with your situation, it’s time to take proactive steps towards seeking guidance and support.

Effective Debt Management Strategies

Regaining control of your debt requires a structured approach and commitment. Here are some actionable strategies for effective debt management.

1. Create a Realistic Budget

Understanding where your money goes is fundamental. Develop a detailed budget that tracks all income and expenses. This will highlight areas where you can cut back and free up funds for debt repayment. Be honest and realistic to ensure sustainability.

2. Prioritise Your Debts

There are two main popular methods for prioritising debt repayment:

- Debt Snowball: Pay off the smallest debt first to gain psychological momentum, while making minimum payments on others.

- Debt Avalanche: Tackle the debt with the highest interest rate first, saving more money over time.

Choose the method that best motivates you.

3. Consider Debt Consolidation

Debt consolidation involves combining multiple debts into a single, often lower-interest loan. This can simplify payments and potentially reduce your overall interest costs. Options include personal loans, balance transfer credit cards, or home equity loans (be cautious as this secures unsecured debt).

4. Negotiate with Creditors

Don’t be afraid to contact your creditors. Many are willing to work with you if you’re proactive. You might be able to negotiate lower interest rates, extended payment plans, or even a partial debt write-off, especially if you can demonstrate genuine hardship.

5. Increase Your Income (If Possible)

Look for opportunities to boost your income, whether through a side hustle, overtime, or selling unused items. Every extra dollar can accelerate your debt repayment journey.

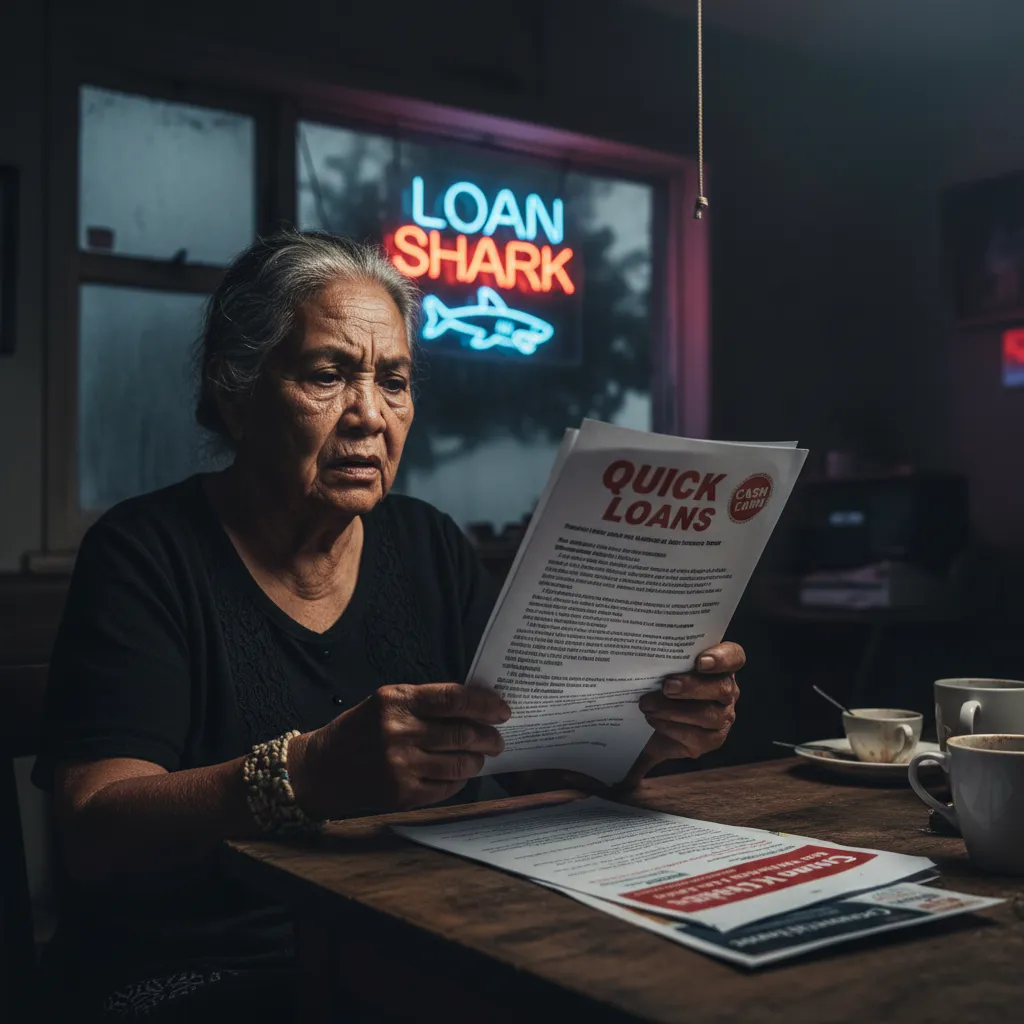

Avoiding Predatory Lending

In times of financial hardship, the lure of quick cash can lead people towards predatory lenders. These lenders often target vulnerable communities, including parts of South Auckland, with loans that have exorbitant interest rates and unfair terms, trapping borrowers in a cycle of debt. Being aware is your best defence.

Stat Callout: Research indicates that New Zealanders who use high-cost, short-term loans can pay back up to three times the original loan amount due to excessive fees and interest, a trap often laid by predatory lenders.

Signs of Predatory Lending:

- Sky-High Interest Rates: Often exceeding 100% or even 500% APR.

- Hidden Fees: Excessive application fees, late payment fees, or rollover fees that inflate the cost.

- Short Repayment Terms: Requiring full repayment in a very short period, making it difficult to meet.

- Pressure Tactics: Aggressive marketing or rushing you to sign without fully understanding the terms.

- No Credit Checks (or Minimal): While seemingly helpful, this often indicates a higher risk that is offset by predatory rates.

If you encounter such an offer, walk away. Always seek advice from trusted community financial services or government-backed resources when looking for debt help South Auckland provides.

Pathways to Debt Relief

When debt becomes unmanageable, there are formal pathways available for relief. These options should be considered with careful thought and often with professional guidance.

Debt Management Plans (DMPs)

A DMP is a formal arrangement facilitated by a non-profit debt advisory service. They negotiate with your creditors on your behalf to combine your unsecured debts into one affordable monthly payment. Creditors may agree to lower interest rates or waive fees, making your payments more manageable. DMPs are a strong option for those seeking structured debt help South Auckland services can provide.

Accessing Community Financial Support

South Auckland is home to numerous community organisations and financial mentoring services that offer free and confidential assistance. These groups can help you budget, negotiate with creditors, and explore all available debt relief options tailored to your specific situation. They are an invaluable local resource.

Stat Callout: A recent study by FINCAP (National Building Financial Capability Charitable Trust) indicated that individuals who receive financial mentoring are significantly more likely to achieve their financial goals and reduce debt within 12 months, highlighting the impact of accessible debt help South Auckland communities provide.

Understanding Bankruptcy and Insolvency

For extreme cases of unmanageable debt, formal insolvency options like bankruptcy or a no-asset procedure (NAP) may be considered. These are serious legal processes that offer a fresh start but come with significant consequences, including impacts on your credit rating and certain restrictions. It is imperative to seek professional legal and financial advice before considering these options.

Your Debt Relief Action Checklist

Take the first steps towards financial freedom with this actionable checklist:

- Review All Debts: List every creditor, amount, interest rate, and minimum payment. Get a complete picture.

- Build a Realistic Budget: Track income and expenses diligently to identify where money goes and where to cut back.

- Cut Unnecessary Spending: Find areas to reduce costs and free up funds for debt repayment.

- Contact Creditors: Proactively discuss potential payment plans or hardship options with your lenders.

- Explore Consolidation: Investigate options like balance transfers or debt consolidation loans (with caution).

- Seek Professional Advice: Connect with a reputable financial advisor or community debt service in South Auckland.

- Educate Yourself: Learn about your rights and available debt relief pathways.

- Stay Consistent: Stick to your plan and review your progress regularly.

Taking control of your debt is a journey, not a sprint. It requires patience, discipline, and the willingness to ask for help. Remember, you don’t have to face your financial struggles alone. There is abundant debt help South Auckland resources offer, designed to support you every step of the way towards financial freedom. Embrace the journey, and commit to building a more secure future for yourself and your whānau.

Frequently Asked Questions About Debt Help in South Auckland

What is the first step to get debt help in South Auckland?

The very first step is to acknowledge the situation and gather all your financial documents. Create a clear picture of what you owe, to whom, and what your monthly income and expenses are. Then, consider reaching out to a local community financial advisor or debt counselling service for tailored advice. This proactive approach is crucial for effective debt help South Auckland.

Are there free debt advisory services available in South Auckland?

Yes, there are several non-profit organisations and community trusts in South Auckland that offer free, confidential financial mentoring and debt advisory services. These services are invaluable for residents seeking debt help South Auckland without incurring further costs. They can guide you through budgeting, debt management plans, and connecting with creditors.

How can I avoid predatory lenders in South Auckland?

To avoid predatory lenders, always be wary of loans with extremely high interest rates, hidden fees, or very short repayment periods. Research the lender’s reputation, read reviews, and check if they are registered with the Financial Service Providers Register (FSPR) in New Zealand. Prioritise reputable, regulated institutions or community-based lending schemes when seeking debt help South Auckland. If an offer seems too good to be true, it likely is.

What is a Debt Management Plan (DMP) and how does it work?

A Debt Management Plan (DMP) is a formal arrangement made through a debt advisory service with your creditors. The service helps you consolidate your unsecured debts into one affordable monthly payment. They then distribute this payment among your creditors. DMPs can often lead to reduced interest rates or waived fees, making repayment more manageable. It’s a structured approach to getting significant debt help South Auckland without resorting to bankruptcy.

References & Sources

- Financial Services Complaints Limited (FSCL). (Ongoing). Consumer Resources on Debt and Lending.

- Ministry of Business, Innovation & Employment (MBIE). (Ongoing). Information on Predatory Lending and Consumer Rights.

- Community Law Aotearoa. (Ongoing). Debt and Money – Your Rights and Options.

- Sorted.org.nz. (Ongoing). New Zealand’s guide to managing your money.

- New Zealand Commerce Commission. (Ongoing). Consumer Credit Law.

- FINCAP (National Building Financial Capability Charitable Trust). (Ongoing). Impact of Financial Mentoring.