Loan & Credit Card Advice

Navigate loans & credit cards with confidence. Learn about responsible lending in NZ, understanding interest rates, and avoiding debt traps for financial resilience.

mangerebudgeting.org.nz

What You Will Learn

Navigate loans & credit cards with confidence. Learn about responsible lending in NZ, understanding interest rates, and avoiding debt traps for financial resilience.

Navigating the world of loans and credit cards can feel overwhelming, especially with complex terms and varying interest rates. For residents of South Auckland, understanding how to make informed financial decisions is crucial for building and maintaining financial resilience. This comprehensive guide from Mangere Budgeting Services is designed to empower you with the knowledge needed to manage credit responsibly, choose appropriate loans, and steer clear of debt traps, all while highlighting the importance of responsible lending in NZ.

Our aim is to demystify financial products, ensuring you feel confident and in control of your financial future. We believe that with the right information, everyone can achieve greater financial stability and peace of mind.

Table of Contents

Choosing Appropriate Loans and Understanding Terms

Loans can be powerful tools to achieve financial goals, whether it’s buying a home, purchasing a car, or consolidating existing debts. However, choosing the right loan requires careful consideration and a thorough understanding of its terms. Missteps here can lead to significant financial strain, underscoring the importance of responsible lending NZ practices and informed borrowing.

1. Assess Your Needs and Capacity

Before even looking at lenders, take an honest look at your financial situation. What is the loan for? How much do you truly need? More importantly, can you comfortably afford the repayments without jeopardising other essential expenses?

- Budget Analysis: Create a detailed budget to understand your income and expenses. This will reveal your disposable income available for loan repayments.

- Emergency Fund: Ensure you have an emergency fund. Relying on a loan for unexpected expenses can quickly lead to a debt cycle.

- Consider Alternatives: Is a loan the only option? Could saving for a few months achieve your goal without incurring interest?

2. Explore Loan Types Safely

Not all loans are created equal. Different types come with varying risks, interest rates, and terms. Being aware of these distinctions is a cornerstone of responsible lending NZ and borrowing.

- Personal Loans: Often unsecured, meaning no asset is used as collateral. Interest rates can be higher, but they offer flexibility.

- Secured Loans: Require an asset (like a car or property) as collateral. These typically have lower interest rates but come with the risk of losing the asset if you default.

- Home Loans/Mortgages: Large, long-term secured loans for property purchase.

- Payday Loans: These are very high-cost, short-term loans. While they offer quick cash, their exorbitant interest rates (often over 500% APR) make them extremely dangerous and should generally be avoided. They are a significant contributor to debt spirals for vulnerable individuals.

3. Decipher Loan Terminology

Understanding the language of loans is paramount. Don’t sign anything you don’t fully comprehend.

- Principal: The initial amount of money you borrow.

- Interest Rate: The cost of borrowing money, expressed as a percentage of the principal.

- Annual Percentage Rate (APR): The total cost of the loan over a year, including the interest rate and any fees. This is a crucial figure for comparing loans.

- Loan Term: The duration over which you will repay the loan. Longer terms often mean lower monthly payments but higher overall interest paid.

- Fees: Be aware of establishment fees, administration fees, late payment fees, and early repayment penalties. These can significantly increase the total cost of your loan.

“The true cost of a loan isn’t just the principal; it’s the principal plus all interest and fees over the entire loan term. Always look at the total amount repayable.”

Managing Credit Cards Responsibly to Avoid Debt Traps

Credit cards, when used wisely, can be convenient financial tools, offering rewards, purchase protection, and a means to build a credit history. However, their ease of use and revolving credit nature also make them potent debt traps if not managed carefully. Mastering credit card management is a vital skill for financial resilience.

1. Understand Credit Card Benefits & Risks

Many New Zealanders underestimate the risks associated with credit cards. For instance, a recent survey found that 1 in 5 New Zealanders are struggling to pay off their credit card debt.

- Benefits: Convenient for online purchases, emergencies, earning rewards (points, cashback), building credit history when used responsibly.

- Risks: High interest rates (often 15-25% p.a. or more), minimum payments can create a debt spiral, tempting to overspend, cash advances come with immediate interest and fees.

2. Strategies for Smart Credit Card Use

To harness the benefits and avoid the pitfalls, adopt these strategies:

- Pay in Full, Every Time: This is the golden rule. If you can’t pay the statement balance in full by the due date, you’ll be charged interest, negating any benefits.

- Set a Realistic Limit: Keep your credit limit lower than what you’re approved for if you know you’re prone to overspending.

- Understand Your Billing Cycle: Know when your statement closes and when payment is due to maximise your interest-free period.

- Avoid Cash Advances: These are essentially high-interest, immediate loans with fees and no interest-free period.

- Monitor Statements: Regularly check your statements for errors, fraudulent charges, and to keep track of your spending.

3. How to Avoid Common Credit Card Debt Traps

Credit card debt can quickly escalate. Be vigilant against these common traps:

- Minimum Payments Only: Paying only the minimum amount can mean it takes decades to clear your debt, paying many times the original purchase amount in interest.

- Balance Transfers Without a Plan: While 0% balance transfers can offer a reprieve, they are only effective if you have a concrete plan to clear the debt before the promotional period ends.

- Using Credit for Everyday Expenses: If you’re relying on a credit card to cover groceries or utilities, it’s a clear sign your budget is out of balance.

Understanding Interest Rates and Fees: The True Cost of Borrowing

Interest rates and fees are the fundamental components that determine the actual cost of any loan or credit card. A clear grasp of how they work is not just beneficial, but essential for making financially sound decisions and adhering to the principles of responsible lending NZ.

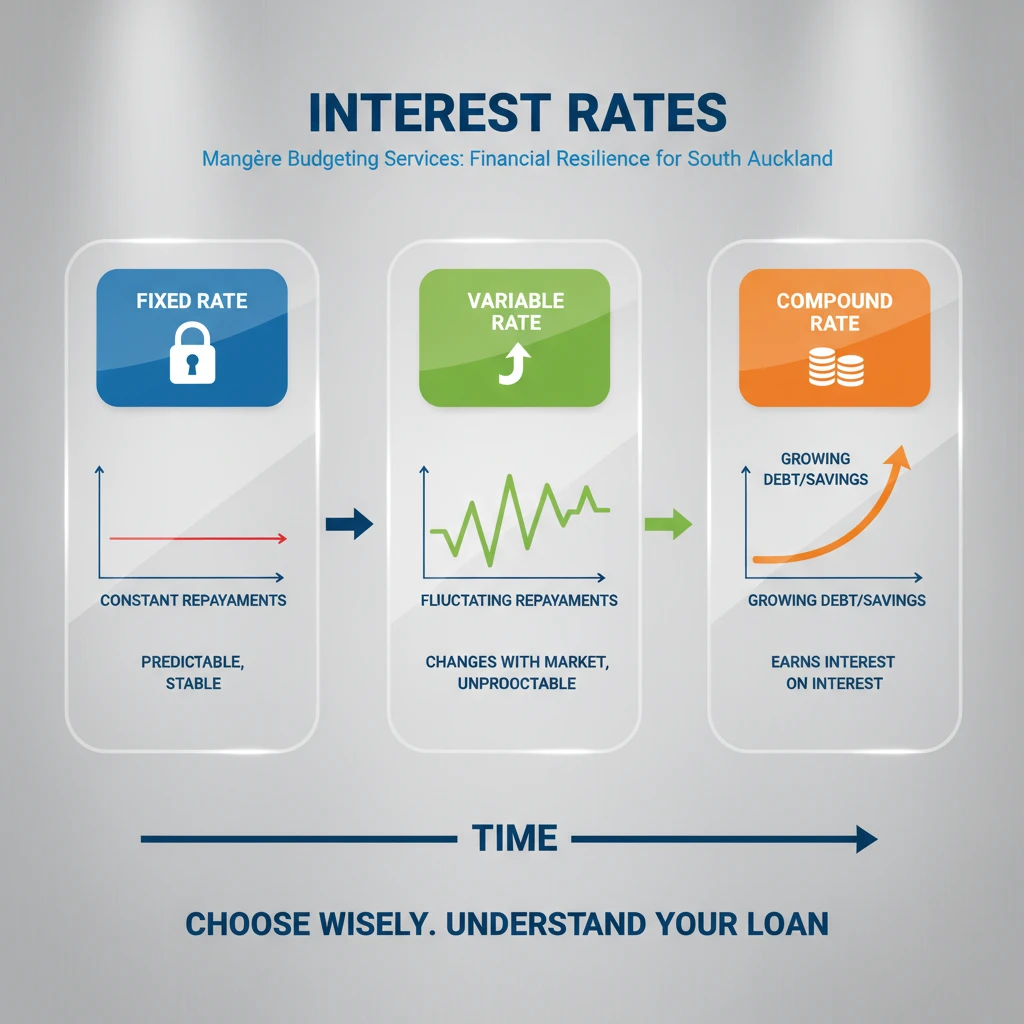

1. Grasping Interest Rate Mechanics

Interest is the price you pay for borrowing money. It’s crucial to understand how it’s calculated and applied.

- Simple Interest: Calculated only on the principal amount of a loan. Used less commonly for consumer loans.

- Compound Interest: Calculated on the initial principal and also on the accumulated interest of previous periods. This is standard for most loans and credit cards, meaning interest can grow on interest.

- Fixed vs. Variable Rates: Fixed rates remain constant throughout the loan term, offering predictability. Variable rates can fluctuate with market conditions, potentially leading to higher or lower payments.

2. Identifying Common Loan Fees

Beyond the interest rate, various fees can significantly add to the cost of borrowing. Always ask for a full breakdown of all fees before committing.

- Establishment/Application Fees: One-off fees charged at the start of a loan.

- Administration/Service Fees: Regular fees (monthly or annually) for managing the loan account.

- Late Payment Fees: Penalties for missing a payment due date. These can be substantial and also negatively impact your credit score.

- Early Repayment Fees: Some loans charge a fee if you pay off your loan ahead of schedule, designed to compensate the lender for lost interest.

- Default Fees: Charges incurred if you fail to meet your loan obligations.

Responsible Lending in NZ: Your Rights and Protections

New Zealand has specific regulations in place to protect borrowers and ensure fair practices from lenders. The Responsible Lending Code is a cornerstone of this framework, guiding how lenders should interact with consumers. Understanding your rights under this code is crucial for anyone seeking loans or credit.

The Responsible Lending Code: What It Means for You

The Responsible Lending Code, part of the Credit Contracts and Consumer Finance Act (CCCFA), outlines what lenders must do when offering credit. This includes:

- Thorough Assessment: Lenders must make reasonable inquiries to ensure the loan is suitable for your purpose and that you can afford the repayments without suffering hardship.

- Clear Information: You must be given clear and concise information about the loan terms, interest rates, fees, and total cost.

- No Undue Pressure: Lenders should not pressure you into taking a loan that is unsuitable or unaffordable.

- Help if You Get into Difficulty: Lenders are expected to engage constructively if you face unexpected hardship and cannot make repayments.

Your Role in Responsible Borrowing

While the code places obligations on lenders, you also have a responsibility as a borrower. This includes being honest about your financial situation, providing accurate information, and actively seeking to understand the terms of any credit contract. If you feel a lender is not adhering to the Responsible Lending Code, you have the right to complain to them and, if unresolved, to an external dispute resolution scheme.

Frequently Asked Questions (FAQ)

- What does responsible lending NZ mean for me as a borrower?

Responsible lending in NZ means lenders must ensure any loan they provide is suitable for your needs and that you can afford the repayments without experiencing significant hardship. They must also provide clear information about the loan’s terms, interest, and fees. As a borrower, it means you should be honest about your financial situation and understand the commitment you’re making.

- How can I improve my chances of getting a loan with a good interest rate?

To improve your chances, focus on maintaining a good credit score by paying bills on time, keeping credit utilisation low, and avoiding too many credit applications in a short period. A stable income, low existing debt, and a clear purpose for the loan also strengthen your application.

- What’s the biggest risk of only paying the minimum on my credit card?

The biggest risk is getting trapped in a long-term debt cycle where a large portion of your payment goes towards interest, not the principal. This means it takes significantly longer and costs much more to clear your debt, potentially leading to financial stress and impacting your ability to save or invest.

- Where can I get help if I’m struggling with debt in South Auckland?

If you’re in South Auckland and struggling with debt, Mangere Budgeting Services offers free, confidential advice and support. We can help you create a budget, negotiate with creditors, and explore debt management options to help you regain control of your finances. You can contact us directly for assistance.

References & Sources

- Commerce Commission New Zealand. (n.d.). Credit Contracts and Consumer Finance Act (CCCFA) and Responsible Lending Code. Retrieved from comcom.govt.nz

- Sorted.org.nz. (n.d.). Loans and Credit. Retrieved from sorted.org.nz

- Financial Services Complaints Limited (FSCL). (n.d.). Understanding responsible lending. Retrieved from fscl.org.nz

- Citizens Advice Bureau NZ. (n.d.). Debt and money problems. Retrieved from cab.org.nz